{kind=link}

Bitcoin was created as a response to the form of debt-financed financial dysfunction now taking part in out throughout international bond markets. The unique thesis was that when governments borrowed recklessly and debased their currencies, hard-money belongings would soak up the ensuing demand.

What that thesis left unresolved is the chance that the debt spiral may tighten monetary situations sturdy sufficient to suppress speculative belongings earlier than the hard-money argument has time to play out.

In 2026, the long-term narrative and the short-term mechanics are operating in reverse instructions, and understanding why requires spending a couple of minutes with essentially the most consequential quantity in international finance proper now.

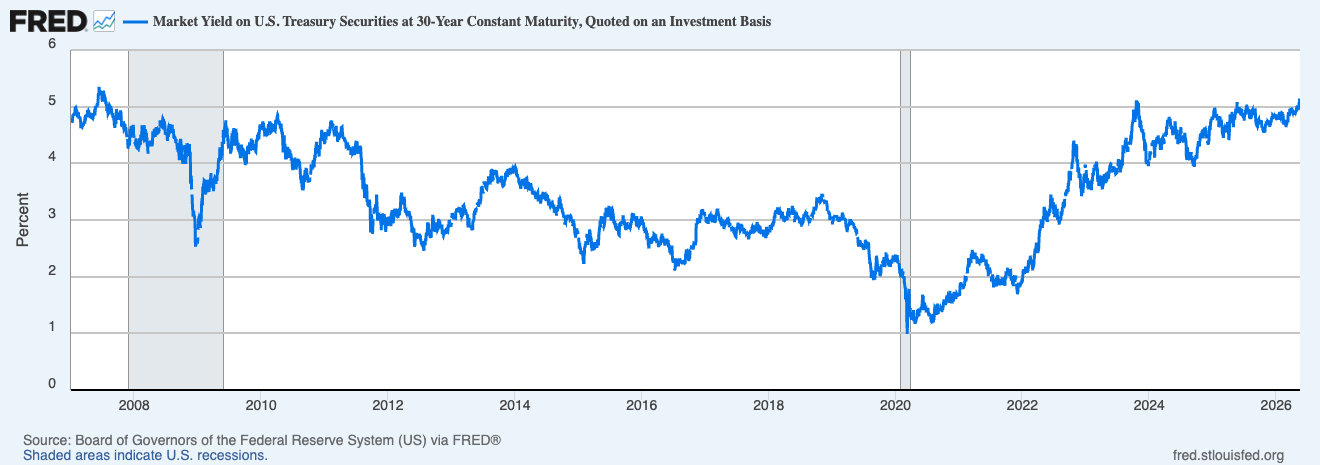

On Might 20, the 30-year Treasury yield reached 5.18%. A $25 billion public sale of latest 30-year bonds on Might 13 was awarded at 5.046%, the primary time traders have obtained 5% on the lengthy bond since 2007, pushed by surging vitality costs and rising expectations that inflation may show extra sturdy than markets assumed.

The final time yields had been at these ranges, Bear Stearns was nonetheless a priority, and quantitative easing was nonetheless a theoretical idea. All the things that is occurred in markets since (the post-2008 period of suppressed charges, central financial institution asset purchases, near-zero borrowing prices) was predicated on yields ultimately coming again down and staying there, and the present repricing is difficult that assumption throughout the complete curve.

America is borrowing cash to pay curiosity on borrowed cash

The inflation drivers behind this transfer are properly documented: US Treasury yields moved greater as traders weighed the implications of extra pricey vitality costs tied to the Iran conflict, with WTI crude settling above $106 a barrel and Brent climbing to $114.44.

Vitality is an actual issue, however the deeper structural pressure (and the one with extra endurance) is the sheer quantity of US authorities debt that needs to be refinanced and issued right into a market that is already repricing inflation danger. The US Treasury will probably have borrowed greater than $2 trillion by the top of the fiscal yr, with the Workplace of Administration and Finances projecting a deficit of $2.06 trillion for FY2026, greater than the Congressional Finances Workplace estimates.

To service that borrowing, the Treasury paid out almost $530 billion in curiosity between October 2025 and March 2026, greater than $88 billion a month, a determine that is roughly equal to spending on each the Division of Protection and the Division of Training mixed.

This drawback feeds on itself. Curiosity funds on the nationwide debt have been 6.1% greater than the earlier yr via the sixth month of FY2026 and have turn into the second-largest spending class within the federal finances, outpacing all finances classes besides Social Safety. The CBO tasks these annual prices climbing from $1 trillion in 2026 to $2.1 trillion by 2036.

In the meantime, the Treasury’s personal borrowing calendar retains upward pressure on the lengthy finish, with $189 billion anticipated within the second quarter and $671 billion within the third, that means the bond selloff has shelf life properly past any particular person Iran headline.

That is what the bond market is definitely pricing: weak international demand, monumental provide, and an inflation backdrop that is giving the Federal Reserve little or no room to maneuver. Futures markets now assign greater than a 44% likelihood of a Fed fee improve by December, a pointy shift from expectations of a number of cuts earlier within the yr. Barclays has moved its first anticipated Fed minimize to March 2027. Fee cuts, which crypto markets spent most of 2024 and 2025 treating as a dependable tailwind, are actually being actively repriced off the desk.

How a Treasury public sale ended up transferring Bitcoin

Bitcoin’s retreat beneath $80,000 final week reveals how rapidly the bond market has reclaimed management of crypto buying and selling, even after lawmakers superior one of many trade’s most intently watched regulatory payments.

The CLARITY Act was anticipated to generate a sustained constructive tone throughout the crypto market.

As a substitute, US spot Bitcoin ETFs noticed roughly 14,000 BTC in weekly outflows, ending a six-week influx streak, as hotter inflation information pressured markets to reassess danger publicity. Spot net-volume on Binance dropped from roughly $50 million to $6.5 million, and on Coinbase from $30 million to $5.7 million.

It is a direct transmission mechanism. An institutional allocator who can now get 5% on a 30-year authorities bond, assured, faces a unique determination than one who was working with 3.5% yields two years in the past. Rising Treasury yields elevate the chance value of holding a risky, non-yielding asset like BTC, making institutional consumers extra selective as authorities debt presents a stronger return profile.

Tokenized US Treasuries have hit a report $15.35 billion in on-chain market worth, up roughly 70% year-to-date, as yield-sensitive capital finds a house that mixes crypto infrastructure with bond-market returns.

That is the structural consequence of the ETF period that CryptoSlate has been monitoring: Bitcoin is now embedded in conventional portfolio allocation frameworks, which suggests it responds to the identical macro inputs as another danger asset. Earlier than ETFs, crypto traded largely by itself inner dynamics, pushed by altcoin rotations, on-chain metrics, and retail sentiment.

As we speak, a Treasury public sale that costs 20 foundation factors above expectations can transfer BTC sooner than any on-chain growth. As CryptoSlate famous in late April, Bitcoin’s restoration rests on renewed institutional inflows and the idea that liquidity situations will not tighten once more. And if Treasuries select a route earlier than that assumption is examined, the bond market may drive Bitcoin’s subsequent transfer independently of any crypto-specific catalyst.

Technique provides one other layer of complexity right here. JPMorgan estimated in early Might that Technique may buy roughly $30 billion in Bitcoin via 2026 if it maintains its present buying tempo, a determine that might put it alongside ETF flows and miner provide as one of many strongest structural forces in Bitcoin’s demand.

The complication is that Technique’s capital construction, which depends on issuing fairness and most well-liked inventory to fund its Bitcoin purchases, turns into dearer to function as yields rise and borrowing prices throughout the system improve. The upper yields climb, the extra the flywheel is determined by sustained investor urge for food for a mannequin that converts yield demand into BTC demand.

The paradox Bitcoin was constructed for

There is a longer argument value holding onto right here, even amid the short-term strain. The rotation out of conventional secure havens into Bitcoin as a perceived different retailer of worth displays the fiat debasement narrative gaining renewed traction as fiscal deficits broaden and central financial institution stability sheets stay structurally massive.

As sovereign debt sustainability issues accumulate and the speed of American borrowing turns into more durable to disregard, the long-cycle argument for Bitcoin as a financial hedge tends to develop alongside it.

Within the close to time period, 5% Treasury yields are a headwind: they tighten monetary situations, elevate the chance value of speculative positions, and drain the marginal liquidity that is traditionally fueled Bitcoin’s bigger rallies.

Throughout an extended horizon, although, the fiscal situations producing these yields, deficits projected to extend from 5.8% of GDP in 2026 to six.7% in 2036, with web curiosity funds rising annually in relation to the dimensions of the economic system, are exactly the situations that make a hard-money, fixed-supply asset like Bitcoin compelling to a rising class of institutional holders.

For years, crypto markets obsessed over the Federal Reserve, watching fee selections and dot plots as the first macro enter. What 2026 is making clear is that the Fed’s room to maneuver is more and more constrained by a bond market pricing in one thing extra sturdy than a brief inflation spike.

The subsequent part of Bitcoin’s trajectory will not depend upon what central bankers determine, however on whether or not international bond traders are starting to lose endurance with the American debt. Which is, should you hint all of it the way in which again, exactly the state of affairs Bitcoin was designed to outlast.