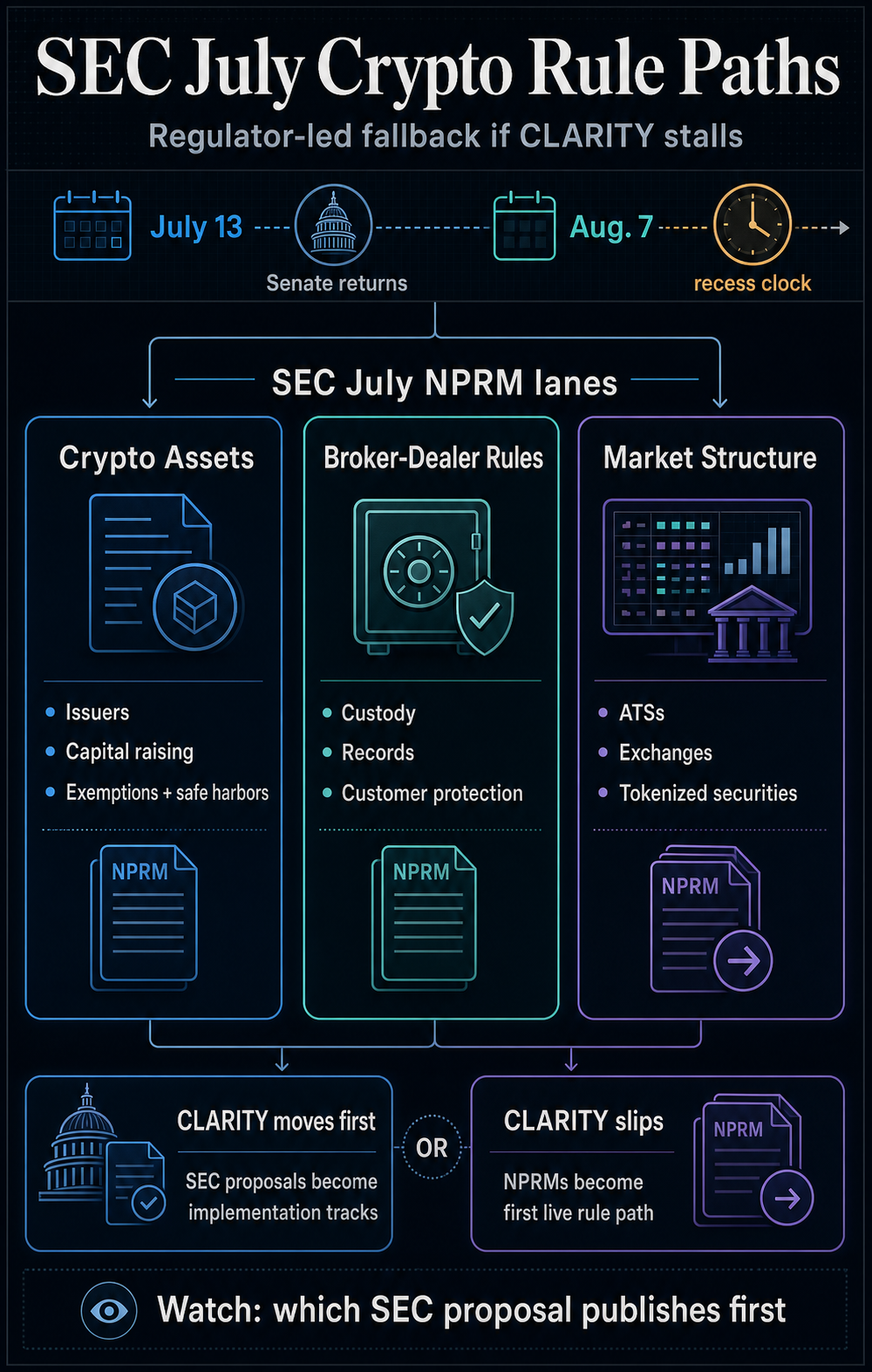

Three SEC crypto proposals are actually penciled in for July, protecting token choices, broker-dealer custody and buying and selling venues. The company might begin writing the foundations earlier than the Senate even decides whether or not to take up the CLARITY Act.

Earlier this week, SEC Chair Paul Atkins mentioned the company’s 2026 regulatory agenda goals to convey extra crypto merchandise onshore, create clearer guidelines for capital elevating with crypto property, and make clear how market contributors can custody and facilitate the buying and selling of tokenized securities on-chain.

In accordance with him:

“[These efforts are to] make sure that the following chapter of monetary management is written within the US, and that our capital markets proceed to steer the world – of their depth, their dynamism, and their unmatched capacity to rework ingenuity into prosperity.”

That posture has translated into three July NPRM targets protecting crypto-asset choices, broker-dealer guidelines, and crypto market-structure amendments.

If any of these proposals is printed this month, the SEC would transfer the crypto debate from coverage signaling into a proper rulemaking course of.

That may come as US lawmakers have but to resolve whether or not to convey the extremely anticipated CLARITY Act to the Senate flooring. The invoice is designed to determine a federal framework for the crypto trade and make clear how oversight is cut up between the SEC and the Commodity Futures Buying and selling Fee.

Whereas CLARITY stays the broader market-structure car, its momentum has slowed because the Senate calendar narrows.

The SEC’s July agenda places the company and Congress on competing tracks. CLARITY would deal with the broader query of who regulates what, whereas the SEC can transfer sooner on issuers, broker-dealers, exchanges and tokenized securities.

SEC’s July agenda targets crypto’s issuance-to-trading pipeline

The SEC has an opportunity to show its July agenda into precise coverage by beginning rulemaking the place crypto most frequently collides with securities legislation: how tokens are issued, how broker-dealers can custody them, and the place they are often traded.

RegInfo’s July goal places crypto fundraising first, with the SEC’s Division of Company Finance weighing new guidelines for the way digital property may be provided and offered.

The entry says these guidelines might embrace exemptions and secure harbors designed to make clear the regulatory framework, present larger market certainty, facilitate capital formation and defend traders.

That may put token issuers and tasks looking for registration, exemption or disclosure paths close to the entrance of the company’s course of. It will additionally transfer one of many trade’s longest-running disputes into a proper rulemaking channel after years by which crypto corporations argued that the SEC relied too closely on enforcement actions.

That is additionally essentially the most legally delicate of the three July entries. RegInfo lists the authorized authority for the Crypto Belongings proposal as “not but decided,” which means the company has not recognized the statutory footing within the agenda entry itself.

That doesn’t preclude a proposal, nevertheless it might turn out to be a degree of assault if the SEC tries to construct a broad providing framework earlier than Congress offers it with clearer authority.

Custody and broker-dealer compliance come subsequent. A separate July entry covers potential amendments to monetary accountability, buyer safety, recordkeeping, and reporting guidelines as they apply to crypto property. The entry cites Guidelines 15c3-1 and 15c3-3, in addition to Guidelines 17a-3 and 17a-4.

These guidelines would form how far regulated securities corporations can go in crypto. Dealer-dealers want clear remedy on capital, custody, buyer safety, and books and data earlier than they’ll help tokenized securities or crypto-linked merchandise throughout regulated platforms.

With out that remedy, Wall Avenue corporations might have demand for crypto merchandise however nonetheless lack the compliance path to deal with them at scale.

The SEC’s third goal covers market construction, with potential Trade Act adjustments governing crypto buying and selling on various buying and selling programs and nationwide securities exchanges.

Collectively, the three July targets present the SEC shouldn’t be solely taking a look at one crypto challenge in isolation. The company is making ready potential rule paths throughout issuance, custody, and buying and selling, which is identical sequence that any regulated crypto market would wish to perform.

A printed SEC proposal would elevate stress on Congress

The race now activates whether or not the SEC can put a crypto proposal into the Federal Register earlier than Congress offers CLARITY a Senate vote.

If the SEC publishes one in every of its July proposals first, the company would give issuers, broker-dealers and buying and selling venues a concrete rulemaking course of to answer whereas the broader market-structure invoice stays unresolved.

The talk would shift from Capitol Hill into SEC rulemaking, giving trade teams an opportunity to argue for broader exemptions and extra workable custody and buying and selling guidelines.

It might additionally change the legislative calculation. A stay SEC proposal might give lawmakers a baseline to just accept, slender or override. It might additionally improve stress on Senate leaders to behave if lawmakers imagine the company is filling gaps that ought to be settled by statute.

Nonetheless, publication alone wouldn’t make the SEC path decisive. The proposals would wish fee approval, public remark and potential revisions earlier than turning into remaining. They may additionally face authorized challenges or be reshaped by any market-structure invoice Congress passes later.

That makes the July agenda essential due to when it might begin, not due to what it may end by itself. It doesn’t substitute CLARITY or settle the complete US crypto rulebook. Nevertheless it offers the SEC a method to start writing securities-side guidelines earlier than the Senate decides whether or not the broader invoice will get flooring time.

The subsequent sign is twofold: whether or not Senate leaders make time for the CLARITY Act earlier than the Aug. 7 recess, and which SEC proposal is printed first.

{kind=link}

If Congress acts first, the SEC’s July agenda might set the equipment of a broader legislation in movement.

If the Senate stalls, the company might begin writing crypto’s securities guidelines earlier than lawmakers vote.