24X Nationwide Trade’s newest tokenized inventory submitting has put Wall Avenue’s core plumbing on the forefront of the equity-tokenization race.

The change filed SR-24X-2026-20 on June 11, with the SEC issuing its discover on June 16 and the June 22 discover putting the submitting within the Federal Register.

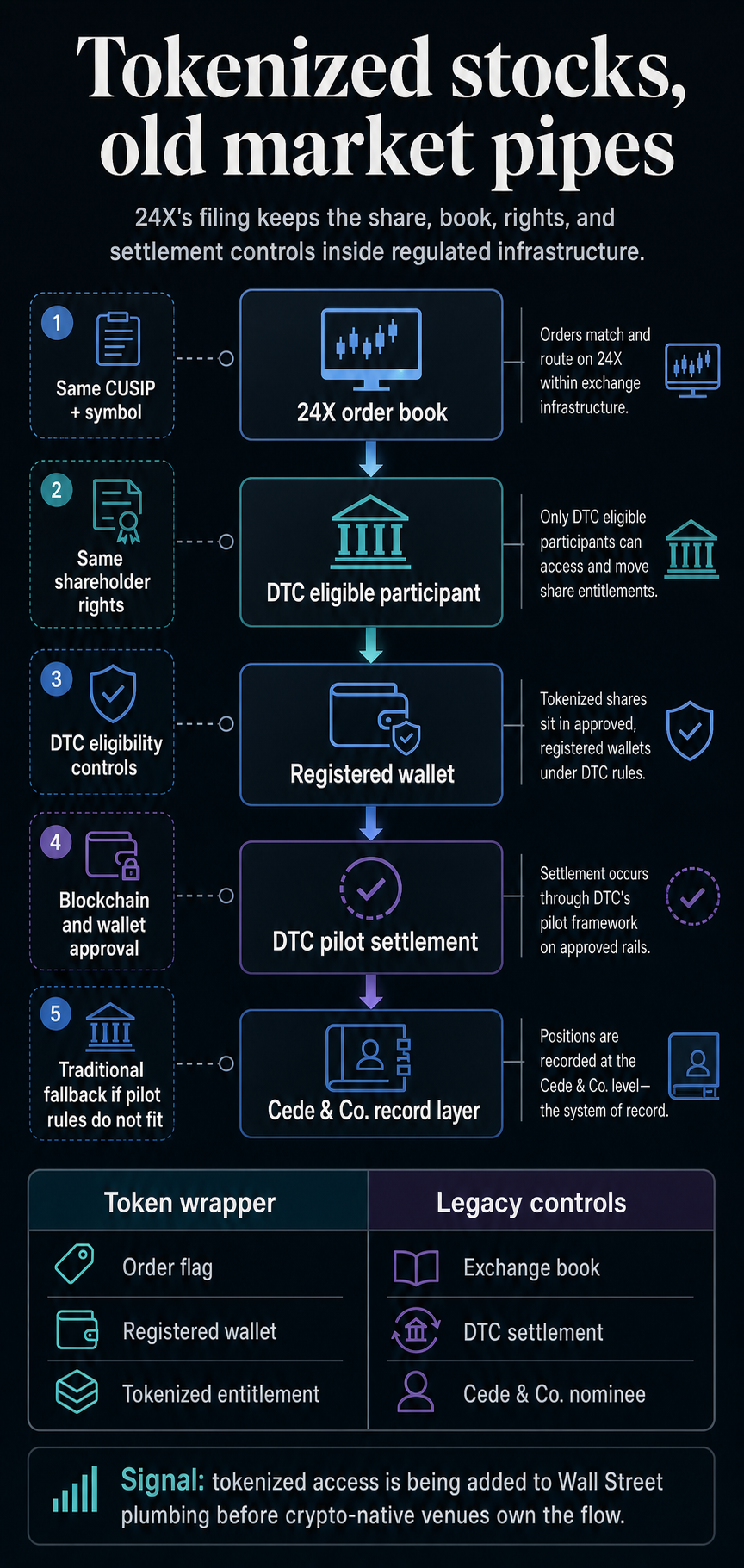

The rule change would let eligible 24X members commerce sure securities in tokenized type throughout a Depository Belief Firm pilot, in line with the SEC’s discover submitting.

The submitting frames tokenization as an improve to the nationwide market system relatively than a workaround. The mannequin described by 24X retains the change, DTC, participant eligibility, order-entry controls, and shareholder-rights protections in place.

The token layer adjustments how eligible positions might be represented and settled, whereas the authorized id of the share and the market construction across the commerce keep intact.

The submitting’s reply is sensible: tokenized shares appear like legacy market infrastructure including a token wrapper.

The token layer stays contained in the market system even with tokenized shares

The submitting would amend 24X guidelines masking eligible securities, member entry, order precedence, and routing. The proposed construction would permit DTC Eligible Individuals to commerce tokenized variations of eligible fairness securities and exchange-traded merchandise on 24X throughout the DTC pilot.

The SEC discover says the securities would commerce throughout the present nationwide market system, utilizing DTC to clear and settle trades in token type based mostly on directions chosen when orders are entered.

That retains tokenized fairness exercise related to the identical market structure that governs peculiar exchange-traded shares.

24X additionally framed the proposal as a part of an exchange-led sample. The submitting says it’s based mostly on an identical Nasdaq proposal that the SEC already authorised.

The authorised Nasdaq precedent exhibits the identical DTC-compatible change mannequin can lengthen throughout nationwide securities exchanges.

That’s the old-pipes-new-token-access stress on the middle of the story. Crypto merchants are used to pondering of tokenization as a strategy to transfer property exterior legacy intermediaries.

The 24X submitting factors in the other way: regulated exchanges are making ready to supply tokenized entry whereas preserving the establishments that already management change buying and selling, custody information, and post-trade settlement.

| Market perform | Tokenized implementation within the submitting | Market-structure impact |

|---|---|---|

| Trade buying and selling | Tokenized and conventional variations commerce on the identical 24X guide | Liquidity stays related to the change guide |

| Safety id | Tokenized shares should share the identical CUSIP, image, rights, and privileges | The token is handled as a type of the identical safety |

| Clearing and settlement | DTC handles token-form settlement throughout the pilot | The post-trade layer stays inside regulated market infrastructure |

| Eligibility controls | Member, safety, blockchain, and pockets eligibility decide whether or not tokenization works | Token entry is permissioned and operationally constrained |

The desk captures the submitting’s central tradeoff: tokenization provides a brand new illustration layer, however every important market perform stays tied to a well-recognized regulated gate.

The token format works solely when change guidelines and DTC methods permit it.

Identical inventory, totally different type

The proposed rule textual content in Exhibit 5 is the strongest proof that 24X is treating tokenization as a type of the identical safety.

Below the proposed language, a safety might commerce in conventional type or, throughout the DTC pilot, in tokenized type.

A tokenized DTC Eligible Safety could be tradable on the identical 24X guide and with the identical execution precedence as the normal model solely whether it is fungible with the normal share, has the identical CUSIP and buying and selling image, and affords the identical rights and privileges.

That rights language is vital. The submitting ties tokenized therapy to the identical rights package deal as the normal safety.

A tokenized instrument that doesn’t carry these rights or share the identical CUSIP and image could be handled as a separate product relatively than a tokenized type of the present share.

The submitting additionally makes tokenization a managed desire. Eligible members that need tokenized settlement would choose a chosen flag at order entry.

That flag might embody DTC-required info, such because the blockchain and pockets handle. 24X would talk the instruction to DTC, however DTC would execute the desire provided that it matches DTC’s guidelines, insurance policies, procedures, and the phrases of the no-action letter.

If the member will not be eligible, the safety will not be eligible, the blockchain will not be appropriate, or the pockets will not be registered with DTC, the order stays in conventional type.

That fallback reveals the management level. The token layer is subordinate to DTC eligibility and change procedures, not the opposite means round.

This creates a sensible boundary for the entire submitting. Tokenized entry can exist, but it surely has to move by way of member eligibility, safety eligibility, pockets registration, blockchain compatibility, and DTC’s personal working limits.

The extra a tokenized product strikes away from these controls, the additional it strays from the route 24X is asking to make use of right here.

DTC retains the file layer shut for tokenized shares

The 24X proposal is determined by DTC’s tokenization pilot, which rests on a Dec. 11, 2025 SEC employees no-action letter.

That letter describes a pilot model of DTCC Tokenization Companies that lets DTC members elect to file safety entitlements to DTC-held securities on a distributed ledger relatively than solely on DTC’s centralized ledger.

The pilot is participant-based. A DTC participant would register a number of authorised blockchain addresses as registered wallets.

If the participant instructs DTC to tokenize an eligible safety entitlement, DTC would debit the entitlement from the participant’s account, credit score it to a Digital Omnibus Account, and mint a token representing that entitlement to the participant’s registered pockets.

Cede & Co., DTC’s nominee, would stay the registered proprietor of the underlying securities represented by tokenized entitlements.

DTC would additionally monitor token actions by way of LedgerScan, an off-chain system that screens pockets exercise and serves as DTC’s official books and information for tokenized entitlements.

That structure provides tokenization some blockchain-like properties whereas preserving the fairness file inside DTC’s managed setting.

Tokens can transfer between registered wallets tied to members, however DTC retains visibility and units know-how requirements.

The pilot additionally consists of limits: eligible securities embody Russell 1000 securities, U.S. Treasuries, and major-index ETFs; tokenized entitlements obtain no collateral or settlement worth for DTC danger controls; DTC should report quarterly to SEC employees; and the employees place withdraws three years after launch except the framework adjustments.

These particulars make the submitting extra consequential. 24X and DTC are constructing a managed path for tokenized entry contained in the equipment that already sits behind U.S. fairness buying and selling.

That managed path nonetheless leaves sensible unknowns for the market. 24X has to establish the eligible securities, DTC has to find out which members, blockchains, and wallets are authorised, and the operational worth has to change into seen to customers who might by no means see the DTC layer immediately.

The actual tokenized inventory contest is distribution

The 24X submitting leaves crypto-native venue seize unresolved. It does, nevertheless, present that regulated venues are constructing a compliant route for tokenized inventory demand earlier than that aggressive query is answered.

The excellence adjustments the aggressive body as a result of the tokenized-equity story has typically been offered as a direct struggle between crypto apps and conventional brokers.

Crypto-native platforms can provide world entry, acquainted pockets interfaces, and always-on person habits. Merchandise that merely monitor inventory costs or depend upon wrappers should go away holders in need of the total rights of a share.

The 24X-DTC mannequin assaults that hole from the opposite route. It preserves the rights and market id of the underlying safety, but it surely does so by preserving entry inside change and DTC controls.

The tradeoff is evident: the mannequin might really feel much less open than a crypto-native product, but it surely retains the share inside a authorized and operational framework acquainted to issuers, brokers, regulators, and establishments.

The DTC pilot sample has already been seen in prior CryptoSlate protection of the DTC tokenization pilot: tokenization is being launched by way of current custody and settlement rails, with restricted eligibility and reporting obligations.

Separate plans from ICE and NYSE level to different incumbent approaches, together with a deliberate tokenized securities platform with always-on and faster-settlement ambitions, however that’s distinct from the 24X submitting’s DTC-pilot construction.

The fast sign from SR-24X-2026-20 is a particular compromise: make the entry tokenized, however preserve the safety, the guide, the rights, and the settlement controls recognizably Wall Avenue.

The subsequent take a look at is whether or not that compromise is helpful sufficient. If DTC-compatible change tokenization delivers significant after-hours entry, world distribution, or operational effectivity with out breaking shareholder rights, legacy infrastructure might personal the primary mainstream model of tokenized equities.

{kind=link}

If it feels too permissioned or too hidden from finish customers, crypto apps will preserve urgent the distribution argument.

For now, the route is forming by way of DTC. Tokenized shares might arrive with a blockchain reference within the order circulate, however the core path nonetheless runs by way of DTC.