{kind=link}

10 Mar Vendor Exhaustion in a ‘Ghost City’ Derivatives Market

Regardless of the twin shocks of the “Black Saturday” geopolitical escalation in Iran two weeks in the past, mixed with a disappointing United States Non-Farm Payrolls (NFP) print displaying the lack of 92,000 jobs, the $60,000–$64,000 flooring for bitcoin has demonstrated surprising resilience. Oil costs shifting practically 80 p.c greater since then will seemingly play a task sooner or later Client Worth Index (CPI) readings, on condition that vitality accounts for about 9 p.c of the ultimate CPI calculation. Such inflationary strain implies there can be headwinds for all danger property.

For bitcoin, nonetheless, two forces are at present at play. The primary is the tendency for BTC to maneuver additional and quicker than different danger property. With its correlation to the upper danger expertise sector growing, whereas its correlation with safe-haven property akin to gold reducing, BTC has seen extra exaggerated draw back strikes earlier than different danger property. Nonetheless, it additionally tends to backside earlier than they do. This dynamic could also be in play now, on condition that BTC has been considerably weaker than the S&P 500 or the NASDAQ for the higher a part of two quarters.

The present regime is finest described because the “Nice Deleveraging.” Retail sentiment stays extremely cautious following a 52 p.c peak-to-trough drawdown from October 2025 highs, and consequently the speculative froth that was within the system has now been virtually totally purged. That is evidenced by the Leverage Reset Index (LRI) — the ratio of mixture open curiosity (OI) to whole change spot reserves — which has hit a multi-year low of 0.32.

This means that worth discovery is now being pushed by bodily spot demand fairly than leveraged derivatives, setting the stage for a high-conviction mean-reversion rally as soon as macro volatility compresses.

1. ETF Movement Regime

The evolution of US spot bitcoin Trade-Traded Fund (ETF) flows gives the clearest proof of an institutional regime shift. The market has moved away from the “Carry Commerce” period of 2024–2025, when hedge funds used ETFs for foundation arbitrage, and right into a “Strategic Allocation” section led by wealth managers and the advisory channel.

March opened with an aggressive three-day enlargement from 2 to 4 March of $1.14 billion in web inflows, solely to be met by a $576.8 million distribution wall on 5–6 March as worth approached the $72,000 vary highs. The session on 9 March confirmed the return of the bid, with a web influx of $167.1 million, although the determine affords restricted encouragement at current.

2. On-Chain Spot Flows: Whale Absorption

On-chain knowledge reveals a big divergence in holder behaviour. Whereas retail cohorts (wallets holding fewer than 10 BTC) have been web sellers for over 30 days, “whales” (entities holding greater than 1,000 BTC) have grown their holdings by 8 p.c because the October peak.

3. The Inflationary Bind

An older research by the Federal Reserve signifies that each sustained $10 improve in oil costs can increase US CPI by 20 foundation factors. This stagflationary menace represents the first headwind for danger property. Ought to oil spike in direction of $120 and stay there, the Federal Reserve would seemingly be compelled right into a hawkish tilt, which might invalidate the restoration thesis. If vitality prices stabilise, nonetheless, the “digital gold” narrative for bitcoin is more likely to strengthen as buyers search sovereign-grade liquidity outdoors the fiat system.

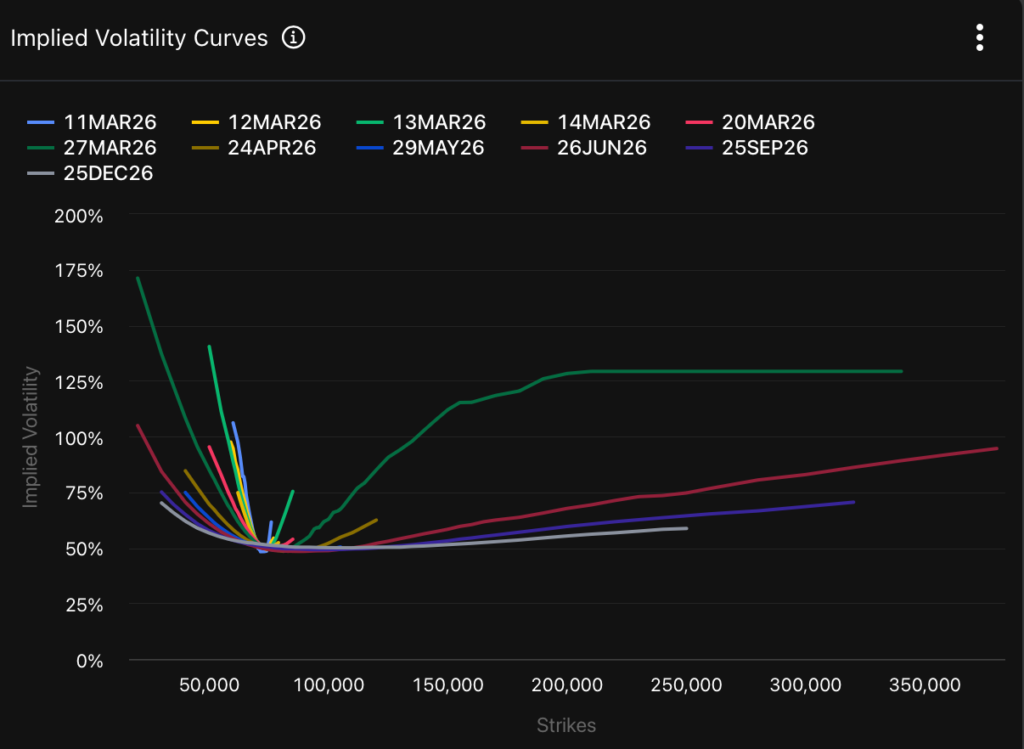

4. Implied Volatility and Time period Construction

At-the-money (ATM) implied volatility for bitcoin choices is at present elevated however not excessive, sitting close to 47 p.c throughout most near- to mid-term maturities. That is considerably decrease than the one hundred pc readings seen in the course of the 2022 bear market, and even the 75–95 p.c spikes witnessed in early February.

The volatility time period construction stays in delicate inversion, with short-dated choices carrying the next premium than longer-dated ones. This can be a traditional signature of a market pricing in near-term uncertainty — seemingly tied to the upcoming Federal Open Market Committee (FOMC) assembly and the continuing Center East battle — whereas sustaining a extra constructive long-term outlook.