Britain’s bond scare is reopening a query Bitcoin was constructed for – moments when belief in sovereign debt and financial administration begins to crack.

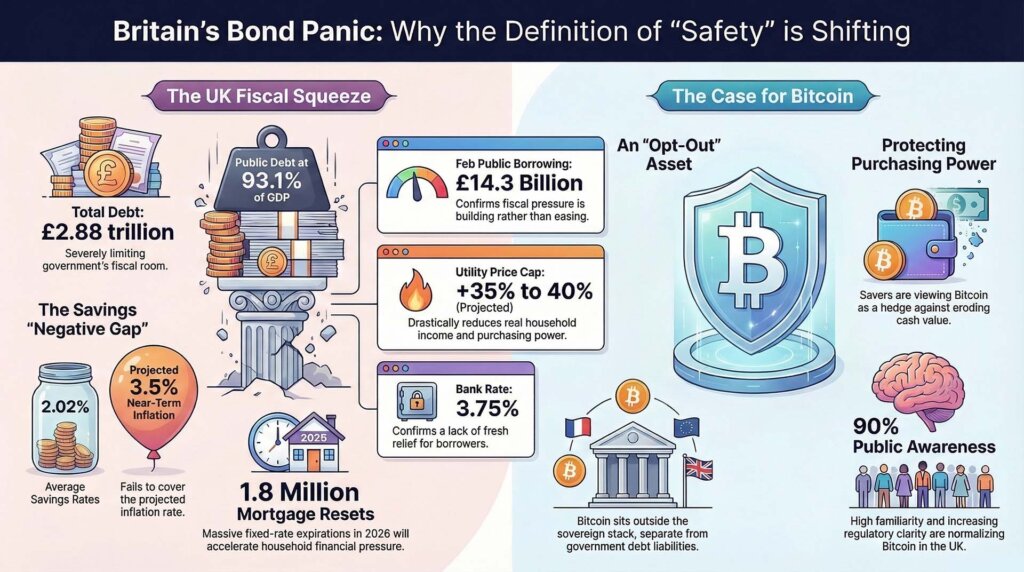

Britain’s fiscal squeeze turned sharper after official borrowing knowledge confirmed February public sector web borrowing hit £14.3 billion, up £2.2 billion from a yr earlier and the second-highest February studying since information started in 1993.

Public sector web debt stood at £2.88 trillion, or 93.1% of GDP. On the identical day, the Financial institution of England held the Financial institution Fee at 3.75% and warned that the newest power shock would push inflation again up over the following couple of quarters whereas elevating family gas and utility prices.

The quick market response sits in gilts, fee expectations, and mortgages. The slower shift reveals up in financial savings conduct. Britain doesn’t want a rush into Bitcoin for the asset to enter the dialog in a brand new approach. A contemporary spherical of doubt about money, authorities bonds, and delayed fee cuts is sufficient to change how savers rank threat.

That shift begins with arithmetic moderately than ideology. The Financial institution of England stated in its newest minutes that preliminary employees estimates now put CPI inflation between 3% and three.5% over the following couple of quarters. It additionally stated larger family gas and utility prices would squeeze actual incomes. By January, the central financial institution’s personal knowledge confirmed the typical fee on family instant-access deposits at 2.02%.

Straightforward-access money is due to this fact paying lower than the inflation vary the Financial institution itself now expects. The hole is apparent, about 0.98 to 1.48 proportion factors under the near-term CPI path. For savers, that’s the place the definition of security begins to shift. Money nonetheless protects nominal worth. It does much less to guard buying energy.

Britain’s family channel can also be shifting shortly. The most recent forecast from UK Finance estimates that about 1.8 million fixed-rate mortgages will finish in 2026. The Workplace for Nationwide Statistics already confirmed in its household-costs index that inflation was working at 3.6% for all households and three.7% for mortgagors within the fourth quarter of 2025. That got here earlier than the Financial institution’s newest warning that power costs would push prices larger once more.

The UK sequence runs by authorities borrowing, gilt repricing, and family budgets. Gilts look much less calm. Straightforward-access money runs under the near-term inflation path. Mortgage ache is ready to hit extra households as mounted offers expire.

Bitcoin features relevance in that setting as savers take into account whether or not a small asset exterior the sovereign stack ought to be included within the combine.

| Indicator | Newest determine | The way it modifications saver conduct |

|---|---|---|

| February public borrowing | £14.3 billion | Exhibits fiscal strain remains to be constructing moderately than easing |

| Public debt | 93.1% of GDP | Limits room for a clear fiscal reset |

| Financial institution Fee | 3.75% | Confirms the Financial institution didn’t ship contemporary aid |

| BoE near-term CPI view | 3% to three.5% | Factors to renewed strain on actual incomes |

| Prompt-access deposit fee | 2.02% | Leaves simple money under the Financial institution’s inflation vary |

| Mortgages resetting in 2026 | 1.8 million | Quickens the family impact of upper charges |

The squeeze begins with money circulate, then reaches portfolio selections

The Financial institution of England’s newest account of the shock provides the cross-market backdrop. In its March assertion, the Financial institution highlighted that round one-fifth of worldwide oil and LNG provide usually passes by the Strait of Hormuz, Brent crude and Dutch TTF gasoline costs had been about 60% above pre-shock ranges, and that UK gasoline futures implied the following Ofgem cap might rise by 35% to 40%.

That’s the bridge between the macro knowledge and the retail saver. A authorities can run a big deficit for years with out altering how households take into consideration cash. Nonetheless, a leap in utility payments lands each month. A mortgage reset lands with a letter and a direct debit. These are the moments when a saver begins evaluating trade-offs throughout buying energy, liquidity, volatility, and belief within the issuer.

The excellence is helpful as Bitcoin fell about 50% from October 2025 to February 2026, whereas choices volatility climbed to its highest degree since 2022. Throughout an energetic squeeze, buyers nonetheless promote unstable property and lift money. Bitcoin stays delicate to liquidity stress in these intervals.

That sample additionally strengthens the longer Bitcoin case on this UK transfer. Gilts are unstable, anticipated fee cuts have moved additional out, and easy-access money yields lower than the inflation the central financial institution now expects. Beneath these situations, Bitcoin begins to look much less like a pure hypothesis and extra like an opt-out from sovereign financial guarantees. It carries its personal volatility and affords a unique supply of threat than the one now confronting money and authorities debt holders.

The regulatory setup within the UK makes that dialogue simpler to have than it was a couple of years in the past. The Monetary Conduct Authority’s newest shopper analysis discovered crypto consciousness above 90%, and 25% of crypto customers stated they’d be extra more likely to make investments if the market had been extra regulated.

The discovering helps familiarity with the asset class and sensitivity to regulatory readability. It leaves the scale and timing of any new demand open.

Britain deserves consideration exterior the UK as a result of the family mechanism is unusually seen. The US nonetheless dominates crypto flows, ETF headlines, and greenback liquidity. But, Britain reveals the strain factors extra shortly.

When debt is excessive, borrowing surprises on the upside, utility payments rise, and a big block of mortgages heads for reset, the query reaches the kitchen desk quicker. The crypto implication is a broader willingness to deal with sovereign paper and financial institution deposits as incomplete solutions to the phrase “protected.”

The official forecasts level in the identical course. In its March outlook, the OBR projected 10-year gilt yields at 4.5% and 30-year yields at 5.3% earlier than this newest shock, whereas additionally seeing public sector web debt rising from 94.5% of GDP in 2025-26 to 96.5% in 2028-29.

It expects the tax burden to rise towards 38% of GDP by 2030-31. These figures level to sustained fiscal pressure and depart little room for a comforting model of the outdated playbook wherein fee cuts, calm bonds, and affected person savers resolve the issue collectively.

{kind=link}

What the following 12 months might appear like

The believable paths for subsequent yr every have a unique impact on financial savings conduct.

The shock fades however doesn’t reverse

The Financial institution’s 3% to three.5% inflation vary proves roughly proper for the following couple of quarters, utility payments rise, and households rebuild precautionary money although actual returns keep comfortable.

In that model, Bitcoin might not appeal to massive flows, although it features narrative floor. The case is straightforward: if money is liquid however dropping buying energy, and bonds are not calm, a non-sovereign asset appears to be like simpler to justify as a part of a broader financial savings combine.

The power shock persists

The Nationwide Institute of Financial and Social Analysis modeled a persistent-shock state of affairs wherein UK inflation runs 0.7 proportion factors larger in 2026, GDP is available in 0.2% decrease in 2026 and 0.3% decrease in 2027, and Financial institution Fee finally ends up about 0.8 proportion factors above baseline.

Earlier than the newest transfer, NIESR’s winter forecast had Financial institution Fee at 3.25% by the top of 2026. Taken collectively, these ranges hold a path above 4% in play if the shock sticks.

That’s the state of affairs more than likely to deepen the Bitcoin case. Excessive debt narrows fiscal room. Sticky inflation cuts into money. Greater-for-longer charges hit mortgages. The mixture will increase curiosity in property that sit exterior the state’s liabilities, even whereas Bitcoin itself stays unstable and delicate to broader market stress.

Market-functioning stress

The third path would hit Bitcoin within the quick run and strengthen its enchantment over an extended interval. NIESR’s separate bond-market notice warns {that a} sovereign period shock can transfer from repricing right into a financial-stability occasion, the place central banks may have market-functioning help even whereas inflation remains to be uncomfortable.

That’s the institutional contradiction Bitcoin was designed to reply. Additionally it is the sort of market interval that may nonetheless strain Bitcoin first if buyers rush for liquidity.

That rigidity explains why Britain’s newest bond transfer stands out. The commerce is messy. The mechanism is obvious. When a state borrows closely, power prices rise, inflation companies once more, and households face mortgage resets, the social that means of security begins to alter. The talk strikes from macro concept to month-to-month outflows and preserved buying energy.

Britain’s newest bond transfer might turn out to be a Bitcoin improvement earlier than many Individuals view it that approach.

The UK knowledge already reveals the substances: £14.3 billion in February borrowing, debt at 93.1% of GDP, a coverage fee held at 3.75%, near-term inflation again at 3% to three.5%, easy-access money at 2.02%, and 1.8 million mortgages resulting from reset in 2026.

None of these figures factors to an instantaneous Bitcoin win. Collectively, they present rising strain on the outdated definition of security.

If power costs keep elevated, if the following utility cap rises as futures indicate, and if mortgage resets hold touchdown right into a interval of excessive gilt yields and delayed fee aid, extra savers might resolve that money and authorities paper not reply the entire drawback.